This is one of a series of posts on fund terms. Other posts include:

Carried Interest Overview

As discussed in my prior post on management fee, the long-standing fee model for private equity funds has been a “2 and 20” model, referring to a 2% management fee and a 20% carried interest. But what is this “carried interest?”

Read on!

Carried interest, also known as “carry,” “profit participation,” “promote” or the "distribution waterfall," is the share of the fund’s profit the fund’s manager (also known as “general partner” or “GP”) earns if the fund returns a profit to the fund’s investors (also known as “limited partners” or “LPs”). See my prior post "LP Corner: US Private Equity Fund Structure - The Limited Partnership" for more detailed descriptions of LPs and the GP.

When a private equity fund calls capital from its LP investors (this is known as “paid-in-capital’ or “called capital” - see my prior post "LP Corner: On Committed Capital, Called Capital and Uncalled Capital" for further discussion of this topic), the GP manager of the fund will use that capital to make investments and to pay for fund expenses, such as management fee. When the investments are realized, the amount in excess of the original investment amount is profit.

The Two types of Carry: Whole Fund and Deal-by-Deal

There are two main types of carry: whole fund carry and deal-by-deal carry.

To read more, please click on the "Read More" link below and to the right.

- Management Fee

- GP Commitment

- Carried Interest – Preferred Return and GP Catchup

- GP Clawback

- Management Fee Offsets

- Key Person Clauses

- No Fault Divorce

- For Cause Actions

- Should Venture Capital Funds have a Preferred Return Hurdle?

Carried Interest Overview

As discussed in my prior post on management fee, the long-standing fee model for private equity funds has been a “2 and 20” model, referring to a 2% management fee and a 20% carried interest. But what is this “carried interest?”

Read on!

Carried interest, also known as “carry,” “profit participation,” “promote” or the "distribution waterfall," is the share of the fund’s profit the fund’s manager (also known as “general partner” or “GP”) earns if the fund returns a profit to the fund’s investors (also known as “limited partners” or “LPs”). See my prior post "LP Corner: US Private Equity Fund Structure - The Limited Partnership" for more detailed descriptions of LPs and the GP.

When a private equity fund calls capital from its LP investors (this is known as “paid-in-capital’ or “called capital” - see my prior post "LP Corner: On Committed Capital, Called Capital and Uncalled Capital" for further discussion of this topic), the GP manager of the fund will use that capital to make investments and to pay for fund expenses, such as management fee. When the investments are realized, the amount in excess of the original investment amount is profit.

The Two types of Carry: Whole Fund and Deal-by-Deal

There are two main types of carry: whole fund carry and deal-by-deal carry.

To read more, please click on the "Read More" link below and to the right.

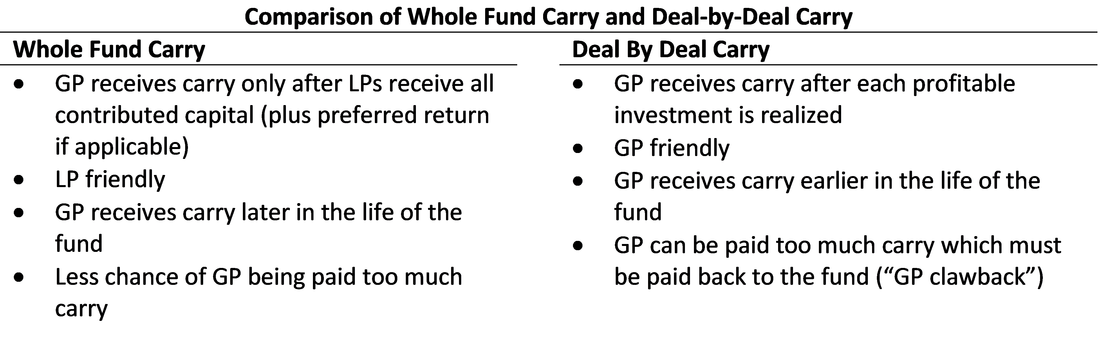

Whole Fund Carry. Whole fund carry (also sometimes known as “European carry” as this type of carry was historically widely used by European funds) provides that the GP receives its carry after the LPs have received back all of their capital contributions (and, if applicable any preferred return – we will discuss preferred return in a later post). Whole fund carry is LP friendly, whereas the deal-by-deal carry is GP friendly.

Deal-by-Deal Carry. Deal-by-deal carry (also sometimes known as “American carry” as this type of carry was used by many American funds) provides that the GP participates in carry as investments (deals) are realized. After a company is sold, if the investment was profitable, the GP will take its 20% carry on this profit. If the deal wasn’t profitable, no carry is taken. Practically speaking, this means the GP will earn carry earlier (and sometimes much earlier) in the life of a fund than whole fund carry. It also means that a GP may (and often is) paid too much carry over the life of the fund, and the GP must repay to the fund the excess carry it was paid. This is called a “GP clawback” and it will be discussed in a later blog post.

Deal-by-Deal Carry. Deal-by-deal carry (also sometimes known as “American carry” as this type of carry was used by many American funds) provides that the GP participates in carry as investments (deals) are realized. After a company is sold, if the investment was profitable, the GP will take its 20% carry on this profit. If the deal wasn’t profitable, no carry is taken. Practically speaking, this means the GP will earn carry earlier (and sometimes much earlier) in the life of a fund than whole fund carry. It also means that a GP may (and often is) paid too much carry over the life of the fund, and the GP must repay to the fund the excess carry it was paid. This is called a “GP clawback” and it will be discussed in a later blog post.

Example

Let’s use a simplified example to illustrate carry. Assume our fund has $100 million of committed capital. To make things easy, we are going to assume the fund has no management fee or expenses and has a 5 year life (these are unrealistic assumptions, but they make the example easier to understand). We also assume that the fund has no preferred return provision (more on this later).

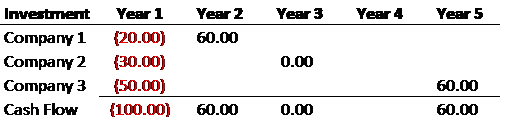

In the first year of the fund, the LPs contribute the entire $100 million to the fund. The fund uses this $100 million to make 3 investments, all in year 1. See the table below:

Let’s use a simplified example to illustrate carry. Assume our fund has $100 million of committed capital. To make things easy, we are going to assume the fund has no management fee or expenses and has a 5 year life (these are unrealistic assumptions, but they make the example easier to understand). We also assume that the fund has no preferred return provision (more on this later).

In the first year of the fund, the LPs contribute the entire $100 million to the fund. The fund uses this $100 million to make 3 investments, all in year 1. See the table below:

The investment amounts are negative and in red because they represent cash outflows from the fund. When the fund sells an investment and receives the money, that amount will appear as a positive number as it will be a cash inflow to the fund.

Let’s now assume that the fund sells Company 1 in year 2 for $60 million. On this investment, the fund realizes a profit of $40 million ($60 million in realizations - $20 million investment). Company 2 doesn’t do well and goes bankrupt in year 3 with the fund losing its entire investment. The fund realizes a net loss of $30 million on its investment in Company 2. Finally, assume that the fund sells Company 3 in year 5 for $60 million. This means the fund realizes a profit of $10 million from its investment in Company 3 ($60 million realized - $50 million invested).

Looking at the cash flows, in year 1, the fund invested $100 million in three companies. The fund received $60 million back when it sold Company 1 in year 2, representing a $40 million profit. The fund lost $30 million when Company 2 went bankrupt in year 3. The fund received $60 million in year 5 when it sold Company 3, for a profit of $10 million.

Now let's look at how the GP will earn carry under each of the whole fund carry model and the deal-by-deal model.

Whole Fund Carry. In our example, the LPs have contributed $100 million in capital. Under whole fund carry, the GP is entitled to carry only after the LPs have received their contributed capital plus any preferred return (if any, and none is assumed in this example). It is only in year 5 when the fund receives $60 million on the sale of Company 3 that the fund can return the contributed capital of $100 million back to the LPs. In our example, over the five-year life of the fund, the fund invested $100 million and realized $120 million, representing a $20 million profit. It is from this $20 million profit that the GP receives its 20% carry, which totals $4 million. The GP receives its carry in year 5. The LPs receive their $100 million in contributed capital back plus their share of the profits, which is $16 million.

Deal-by-Deal Carry. In deal by deal carry, each transaction is looked at and carry is paid on the profits of each transaction. In our example, the fund invested $20 million in Company 1 and in year 2 realized $60 million, for a profit of $40 million. Under deal-by-deal carry, the GP is entitled to its 20% carry from this $40 million profit, for a total carry paid to the GP in year 2 of $8 million. Compare this to whole fund carry – under whole fund carry the GP receives its carry in year 5, and receives total carry of $4 million. Under deal-by-deal carry, the GP receives carry in year 2, and because its investment in Company 1 was very successful, the GP receives $8 million in carry. We will see that ultimately the GP is only entitled to $4 million in carry, and so the GP has been overpaid carry and will have to return the excess to the fund.

Continuing our deal-by-deal carry example, Company 2 went bankrupt, so there’s no profit and no carry. So after two deals, by year 3 the fund has invested $50 million and received back $60 million, for a total profit of $10 million. This means that for these two deals the carry paid to the GP should be $2 million, but since the investment in Company 1 performed so well, the GP has received too much carry. Company 3 is sold in year 5 for $60 million on a $50 million investment, for a profit of $10 million. The GP is entitled to its 20% carry on the $10 million for $2 million. So overall, the GP receives $10 million in carry under the deal-by-deal carry structure.

But wait a minute. The total profit of the fund is $20 million, and so the GPs share of the total profit is $4 million, not $10 million. The GP has received too much carry in our example. What happens when the GP is paid too much carry during the life of the fund is that the GP must return the excess carry to the fund. This is known as a “GP clawback” as the excess carry is “clawed back” from the GP. But there’s another problem – in year 2 when the GP received the $8 million in carry, each partner of the GP that received a share of the carry paid taxes on the amount of the carry, so if they then have to give the money back, they are typically only required to pay the carry back “net of taxes.” This means that when a clawback occurs, the full amount of the over-payment is not paid back, and the LPs are effectively penalized.

Additional Notes:

Let’s now assume that the fund sells Company 1 in year 2 for $60 million. On this investment, the fund realizes a profit of $40 million ($60 million in realizations - $20 million investment). Company 2 doesn’t do well and goes bankrupt in year 3 with the fund losing its entire investment. The fund realizes a net loss of $30 million on its investment in Company 2. Finally, assume that the fund sells Company 3 in year 5 for $60 million. This means the fund realizes a profit of $10 million from its investment in Company 3 ($60 million realized - $50 million invested).

Looking at the cash flows, in year 1, the fund invested $100 million in three companies. The fund received $60 million back when it sold Company 1 in year 2, representing a $40 million profit. The fund lost $30 million when Company 2 went bankrupt in year 3. The fund received $60 million in year 5 when it sold Company 3, for a profit of $10 million.

Now let's look at how the GP will earn carry under each of the whole fund carry model and the deal-by-deal model.

Whole Fund Carry. In our example, the LPs have contributed $100 million in capital. Under whole fund carry, the GP is entitled to carry only after the LPs have received their contributed capital plus any preferred return (if any, and none is assumed in this example). It is only in year 5 when the fund receives $60 million on the sale of Company 3 that the fund can return the contributed capital of $100 million back to the LPs. In our example, over the five-year life of the fund, the fund invested $100 million and realized $120 million, representing a $20 million profit. It is from this $20 million profit that the GP receives its 20% carry, which totals $4 million. The GP receives its carry in year 5. The LPs receive their $100 million in contributed capital back plus their share of the profits, which is $16 million.

Deal-by-Deal Carry. In deal by deal carry, each transaction is looked at and carry is paid on the profits of each transaction. In our example, the fund invested $20 million in Company 1 and in year 2 realized $60 million, for a profit of $40 million. Under deal-by-deal carry, the GP is entitled to its 20% carry from this $40 million profit, for a total carry paid to the GP in year 2 of $8 million. Compare this to whole fund carry – under whole fund carry the GP receives its carry in year 5, and receives total carry of $4 million. Under deal-by-deal carry, the GP receives carry in year 2, and because its investment in Company 1 was very successful, the GP receives $8 million in carry. We will see that ultimately the GP is only entitled to $4 million in carry, and so the GP has been overpaid carry and will have to return the excess to the fund.

Continuing our deal-by-deal carry example, Company 2 went bankrupt, so there’s no profit and no carry. So after two deals, by year 3 the fund has invested $50 million and received back $60 million, for a total profit of $10 million. This means that for these two deals the carry paid to the GP should be $2 million, but since the investment in Company 1 performed so well, the GP has received too much carry. Company 3 is sold in year 5 for $60 million on a $50 million investment, for a profit of $10 million. The GP is entitled to its 20% carry on the $10 million for $2 million. So overall, the GP receives $10 million in carry under the deal-by-deal carry structure.

But wait a minute. The total profit of the fund is $20 million, and so the GPs share of the total profit is $4 million, not $10 million. The GP has received too much carry in our example. What happens when the GP is paid too much carry during the life of the fund is that the GP must return the excess carry to the fund. This is known as a “GP clawback” as the excess carry is “clawed back” from the GP. But there’s another problem – in year 2 when the GP received the $8 million in carry, each partner of the GP that received a share of the carry paid taxes on the amount of the carry, so if they then have to give the money back, they are typically only required to pay the carry back “net of taxes.” This means that when a clawback occurs, the full amount of the over-payment is not paid back, and the LPs are effectively penalized.

Additional Notes:

- Hybrid Carry. Some funds have used variations of the whole fund and deal-by-deal carry models to create what are known as "hybrid carry" models. For example, one variation of a whole fund model might be that rather than being paid carry after all of the LP contributed capital is paid back, carry can be paid after 70% of the LP contributed capital is paid back. This way, the GP will receive carry earlier in the life of the fund. If the hybrid carry structures result in the GP receiving carry earlier than in the whole fund carry model, then the problem of overpaying carry to the GP exists.

- Preferred Return Hurdle. In a later post, we will discuss preferred return hurdles. Essentially, a preferred return adds an additional threshold that the GP must achieve before it can be paid carry. Preferred return hurdles are typically 8% per annum and are universal on buyout funds, common in growth funds, and less common in venture capital funds.

- GP Catch-up. This concept is tied to preferred return hurdle. Once the GP has achieved the preferred return hurdle, it can either be paid on the next dollars of profit, or once the hurdle is met, the GP can be paid carry on all profit, whether above or below the hurdle. This is called the GP catch up, because the GP is either paid all or substantially all of the future profits until it has "caught up" to its full 20% of the fund's profits. This will be discussed in more detail in a later post.

- GP Clawback. If a GP is paid too much carry over the life of a fund, it will have to pay that excess carry back to the fund. This usually occurs at the end of a fund's life, but can also occur earlier or upon certain defined events. GP clawback will be discussed in more detail in a later post.

- Premium Carry. Some funds, notably premier venture capital funds, charge carry in excess of 20%. Some funds charge carry at 25%, a very few charge carry at 30%. Often, a premium carry is only achieved after some hurdle is met (such as a return of 3x of contributed capital), and then the carry is only obtained on the amount in excess of the hurdle.

- Fee Options. Some funds will offer LPs their choice of a fee/carry structure. For example, a fund may offer LPs their choice of (1) management fee of 2% and carry of 20% (standard terms), or (2) management fee of 1% and carry of 30%. By offering options, LPs are able to choose the fee structure that they believe will provide them with the best overall economics.