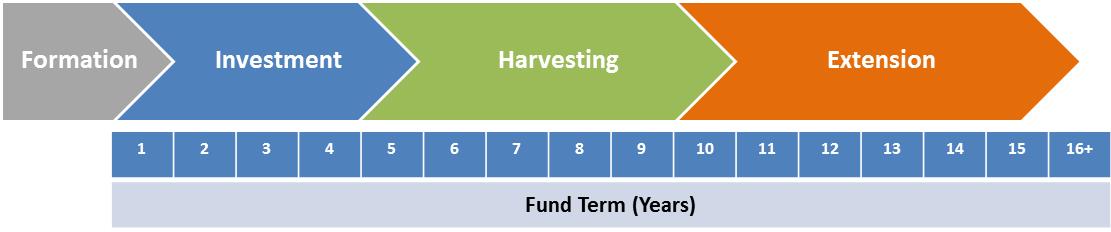

Investing in private equity funds is a long-term process. Private equity funds have finite lives, unlike mutual funds. Most private equity funds come to market with a 10 year term with up to two one-year extensions at the discretion of the manager. This suggests a fund term of 10-12 years. However, most funds exist for much longer than 12 years from the initial call of capital to final liquidation.

I view the life of a private equity fund as having four phases:

- Formation;

- Investment;

- Harvesting; and

- Extension.

The four phases of a fund’s life can be viewed graphically:

To read more, please click on "Read More" to the lower right.