Capitalization tables, also known as “cap tables” show a company’s ownership, and are critical documents for companies. Cap tables are also very important for investors to understand, as they show a snapshot of a company’s ownership at a specific date. Cap tables can be on an “outstanding” share basis or on a “fully-diluted” share basis, and range from very simple to incredibly complex.

Let's get started.

Let's get started.

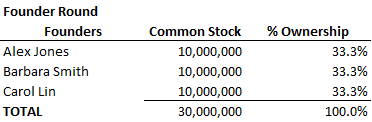

Let’s use the company Lattamattic as an example. Lattamattic was founded by three college classmates, Alex Jones, Barbara Smith and Carol Lin. They each pitch in $1,000 and purchase shares of common stock at $0.001 per share. Because these shares are issued to founders, they are often called “Founders Shares.” The reason for the very low price per share is that at formation, Lattamattic had no real value, except for the $3,000 that the founders contributed. Also, starting at a very low founder price per share means that as they bring in new investors at higher prices, they minimize their dilution. For more on dilution, see the posts “Dilution Part One: Understanding Ownership Dilution” and “Dilution Part Two: Value Dilution.” Here’s the initial cap table:

The above cap table is simple enough. Three stockholders who each own one million shares. As an aside, the “pre-money valuation” for the firm is zero, because there was nothing there. After the founders invested the $3,000, the “post-money” valuation is $3,000. Remember the equation:

Post-Money Valuation = Pre-Money Valuation + Amount Raised

For more on pre- and post-money valuation, see the post “Pre-Money and Post-Money Valuation.”

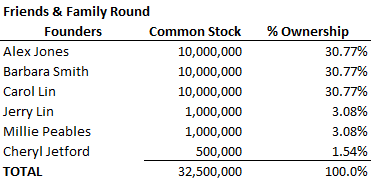

Friends & Family Financing

Lattamattic’s founders develop a limited beta version of the software. The company needs to raise money to build out the software and hire part-time coders to help. They want to raise $250,000 from friends and family. They demo the software to a few family members and close friends, and Carol’s uncle Jerry Lin decides to invest $100,000, Alex’s aunt Millie Peables invests $100,000, and a wealthy friend of Barbara’s, Cheryl Jetford invests $50,000. These “friends and family” investors purchase shares of common stock at $0.10 per share (a 1000x markup to the $0.0001 per share paid by the founders).

Here’s the cap table after the friends and family round:

Post-Money Valuation = Pre-Money Valuation + Amount Raised

For more on pre- and post-money valuation, see the post “Pre-Money and Post-Money Valuation.”

Friends & Family Financing

Lattamattic’s founders develop a limited beta version of the software. The company needs to raise money to build out the software and hire part-time coders to help. They want to raise $250,000 from friends and family. They demo the software to a few family members and close friends, and Carol’s uncle Jerry Lin decides to invest $100,000, Alex’s aunt Millie Peables invests $100,000, and a wealthy friend of Barbara’s, Cheryl Jetford invests $50,000. These “friends and family” investors purchase shares of common stock at $0.10 per share (a 1000x markup to the $0.0001 per share paid by the founders).

Here’s the cap table after the friends and family round:

A couple of notes:

Post-$ Valuation = Financing Proceeds / Post-Financing Ownership Percentage

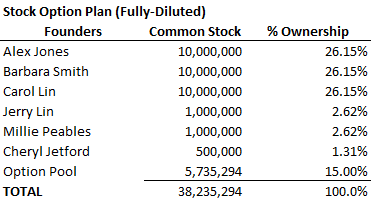

Option Pool

After the Friends & Family financing round, Lattamattic decides to establish a stock option pool so they can grant stock options to employees and consultants. Stock option plans generally run between 10% and 20% of a company’s fully diluted-equity. For more on stock options, see the post “Private Company Stock Option Plans: An Overview for Investors.” For a discussion of fully-diluted equity, see the post “Convertible Preferred Stock: Understanding the Conversion Feature.” Lattamattic decides to go with a 15% stock option pool. The cap table now looks like this:

- The friends and family investors receive ~7.7% of the company for their $250,000 investment.

- The founders’ ownership is diluted from 100% to ~92.3%.

- The post-money valuation is $3.25 million. Recall that the equation for calculating post-money valuation from the financing round information is:

Post-$ Valuation = Financing Proceeds / Post-Financing Ownership Percentage

- The pre-$ valuation (the value of the company immediately prior to the friends and family financing) is $3 million ($3.25 million post-$ valuation minus $325,000 financing proceeds)

Option Pool

After the Friends & Family financing round, Lattamattic decides to establish a stock option pool so they can grant stock options to employees and consultants. Stock option plans generally run between 10% and 20% of a company’s fully diluted-equity. For more on stock options, see the post “Private Company Stock Option Plans: An Overview for Investors.” For a discussion of fully-diluted equity, see the post “Convertible Preferred Stock: Understanding the Conversion Feature.” Lattamattic decides to go with a 15% stock option pool. The cap table now looks like this:

How did we calculate the size of the stock option pool? Using some algebra. If you’re curious, the methodology appears at the end of this post.

One issue is that the above cap table includes all of shares allocated to the stock option plan. But at this point in time, no stock options have been granted. So shouldn’t the number in the cap table be ZERO because no stock options have been granted? Yes and no.

Recall that a company allocates shares to the stock option plan – these are known as the stock option plan’s authorized shares. Once stock options have been granted, the option holder has a right, assuming certain conditions are met, to exercise the option and purchase the shares. This means there are three steps: (1) the company’s board of directors adopts a stock option plan and specifies how many shares of common stock are authorized under the plan; (2) the board of directors then grants options to employees, board members, advisors and consultants; and (3) options are exercised.

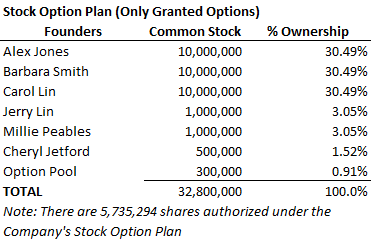

Many companies only include stock options that have been granted in the stock option pool line in the cap table, and either footnote the total authorized shares in the stock option plan or have a separate table showing the stock option plan. If Lattamattic took this approach, and had granted 300,000 stock options, the cap table would look like this:

One issue is that the above cap table includes all of shares allocated to the stock option plan. But at this point in time, no stock options have been granted. So shouldn’t the number in the cap table be ZERO because no stock options have been granted? Yes and no.

Recall that a company allocates shares to the stock option plan – these are known as the stock option plan’s authorized shares. Once stock options have been granted, the option holder has a right, assuming certain conditions are met, to exercise the option and purchase the shares. This means there are three steps: (1) the company’s board of directors adopts a stock option plan and specifies how many shares of common stock are authorized under the plan; (2) the board of directors then grants options to employees, board members, advisors and consultants; and (3) options are exercised.

Many companies only include stock options that have been granted in the stock option pool line in the cap table, and either footnote the total authorized shares in the stock option plan or have a separate table showing the stock option plan. If Lattamattic took this approach, and had granted 300,000 stock options, the cap table would look like this:

AS AN INVESTOR, I want to know how much I will be diluted if the board of directors grants all of the options authorized under the stock option plan. We will include the total authorized stock options in the cap table for Lattamattic, which means the cap table looks like this (which is the same as the first table with options):

Notice the difference between the two above cap tables. With only 300,000 options granted, Alex Jones owns 30.5% of the outstanding stock (top table). But once all of the options are granted (bottom table) Alex will own 26.15% of the company. This demonstrates the impact of stock option plans.

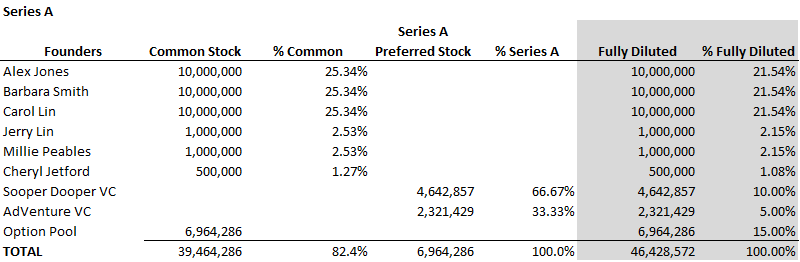

Series A Financing

Lattamattic continues to build the software and soon has a fully working version that is ready to sell to customers. The company now wants to raise $3 million in a Series A preferred stock financing from venture capitalists (“VCs”) to bring on more staff to fuel the growth. The company receives lots of interest from VCs, and accepts $2 million from Super Dooper VC and $1 million from AdVenture VC at a $20 million post-$ valuation. The terms for the Series A preferred stock financing include convertible into common stock, a 1x liquidation preference and a weighted average anti-dilution provision. The Series A investors also require the company to refresh the stock option pool so that it equals 15% of the post-money capitalization.

The cap table becomes more complicated now that we’re introducing convertible preferred stock that can convert into common stock. Because the Series A is convertible, the initial conversion ratio is 1:1, so unless there’s a later adjustment to this ratio (which can occur if there’s a down financing round and if certain other events occur), each share of Series A initially converts into one share of Common Stock.

Series A Financing

Lattamattic continues to build the software and soon has a fully working version that is ready to sell to customers. The company now wants to raise $3 million in a Series A preferred stock financing from venture capitalists (“VCs”) to bring on more staff to fuel the growth. The company receives lots of interest from VCs, and accepts $2 million from Super Dooper VC and $1 million from AdVenture VC at a $20 million post-$ valuation. The terms for the Series A preferred stock financing include convertible into common stock, a 1x liquidation preference and a weighted average anti-dilution provision. The Series A investors also require the company to refresh the stock option pool so that it equals 15% of the post-money capitalization.

The cap table becomes more complicated now that we’re introducing convertible preferred stock that can convert into common stock. Because the Series A is convertible, the initial conversion ratio is 1:1, so unless there’s a later adjustment to this ratio (which can occur if there’s a down financing round and if certain other events occur), each share of Series A initially converts into one share of Common Stock.

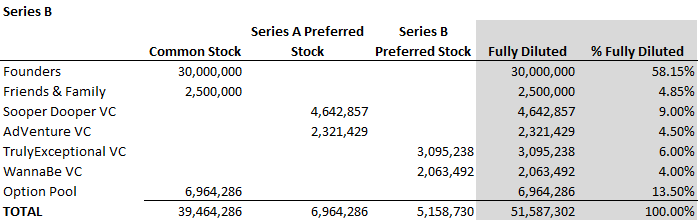

Series B Financing

Lattamattic continues to be successful and soon raises a $50 million Series B convertible preferred financing led by TrulyExceptional VC investing $30 million and WannaBe VC investing $20 million at a $500 million post-$ valuation. Here’s the post-$ cap table:

Lattamattic continues to be successful and soon raises a $50 million Series B convertible preferred financing led by TrulyExceptional VC investing $30 million and WannaBe VC investing $20 million at a $500 million post-$ valuation. Here’s the post-$ cap table:

The founders now own 58% of the company on a fully-diluted basis. Because the company was valued at $500 million post-Series B financing, this means that the founders collectively are worth nearly $300 million dollars. Also, because the option pool wasn’t “refreshed” as part of this round, the stock option plan now represents 13.5% of the fully-diluted shares, down from 15% after the Series A financing.

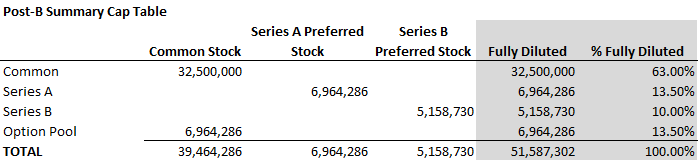

Note that the cap table has changed. As the cap table became more complex, I’ve consolidated the founders into a “founders” line and the friends and family investors into a “Friends and Family” line to make it easier to read.

A summary cap table may combine all common stock holders together in a “common stock” line, combine the Series A investors in a “Series A” line and the Series B investors in a Series B line. Here’s what the summary cap table for Lattamattic would look like:

Note that the cap table has changed. As the cap table became more complex, I’ve consolidated the founders into a “founders” line and the friends and family investors into a “Friends and Family” line to make it easier to read.

A summary cap table may combine all common stock holders together in a “common stock” line, combine the Series A investors in a “Series A” line and the Series B investors in a Series B line. Here’s what the summary cap table for Lattamattic would look like:

So that’s an overview of cap tables.

Notes and Take-Aways:

++++++++++++++++++++

Methodology: Calculating the Size of the Stock Option Pool

This explains how we derived the size of the initial stock option pool.

We know that after the stock option pool is added that it will be 15% of the fully-diluted equity. So let P = Stock Option Pool and FD = Fully-Diluted Equity. This means that P = .15FD (the stock option pool is .15 or 15% of the fully-diluted equity after the stock option pool is added). We also know that the existing equity plus the stock option pool will equal the fully-diluted equity. Let E = existing equity. This means that E + P = FD. Using algebra and solving for P, we get:

P = .15FD

Substituting FD for E+P (recall E+P = FD) we get

P = .15(E+P), which equals P = .15E + .15P

Subtracting .15P from each side of the equation gives us

P – .15P = .15E or

.85P = .15E.

Dividing both sides by .85 gives us

P = (.15/.85)*E or

P = (3/17)*E

Plugging in E (which is existing shares prior to the addition of the pool, or 32,500,000 shares) gives us

P = (3/17)*32,500,000 or

P = 5,735,294

The generic formula is:

P = ((Pool Size as a % of Fully Diluted)/(1-Pool Size))*E

Where:

P = the number of shares allocated to the Stock Option Pool

E = the existing number of shares (before the addition of the pool)

© Allen J. Latta. All rights reserved.

Notes and Take-Aways:

- Cap tables come in all sizes and flavors, from “summary” to incredibly complex.

- Investors want the cap table to show all authorized stock options to understand the total dilution if all of the options are issued and exercised.

- Cap tables used to be created on Excel, and many companies continue to use Excel for their cap tables. However, there are now many online cap table providers. Carta is probably the largest and best known of a crowded field.

++++++++++++++++++++

Methodology: Calculating the Size of the Stock Option Pool

This explains how we derived the size of the initial stock option pool.

We know that after the stock option pool is added that it will be 15% of the fully-diluted equity. So let P = Stock Option Pool and FD = Fully-Diluted Equity. This means that P = .15FD (the stock option pool is .15 or 15% of the fully-diluted equity after the stock option pool is added). We also know that the existing equity plus the stock option pool will equal the fully-diluted equity. Let E = existing equity. This means that E + P = FD. Using algebra and solving for P, we get:

P = .15FD

Substituting FD for E+P (recall E+P = FD) we get

P = .15(E+P), which equals P = .15E + .15P

Subtracting .15P from each side of the equation gives us

P – .15P = .15E or

.85P = .15E.

Dividing both sides by .85 gives us

P = (.15/.85)*E or

P = (3/17)*E

Plugging in E (which is existing shares prior to the addition of the pool, or 32,500,000 shares) gives us

P = (3/17)*32,500,000 or

P = 5,735,294

The generic formula is:

P = ((Pool Size as a % of Fully Diluted)/(1-Pool Size))*E

Where:

P = the number of shares allocated to the Stock Option Pool

E = the existing number of shares (before the addition of the pool)

© Allen J. Latta. All rights reserved.