Overview

Private equity funds-of-funds (“FOFs”) are funds that invest in other private equity funds, which then invest directly into privately-held companies. By investing in a FOF, a limited partner (“LP”) obtains a diversified portfolio of private equity fund investments as well as a larger portfolio of indirect investments in underlying private companies. I have worked for two private equity fund-of-fund managers and understand well the pros and cons of these vehicles. This post provides an overview of FOFs.

Structure

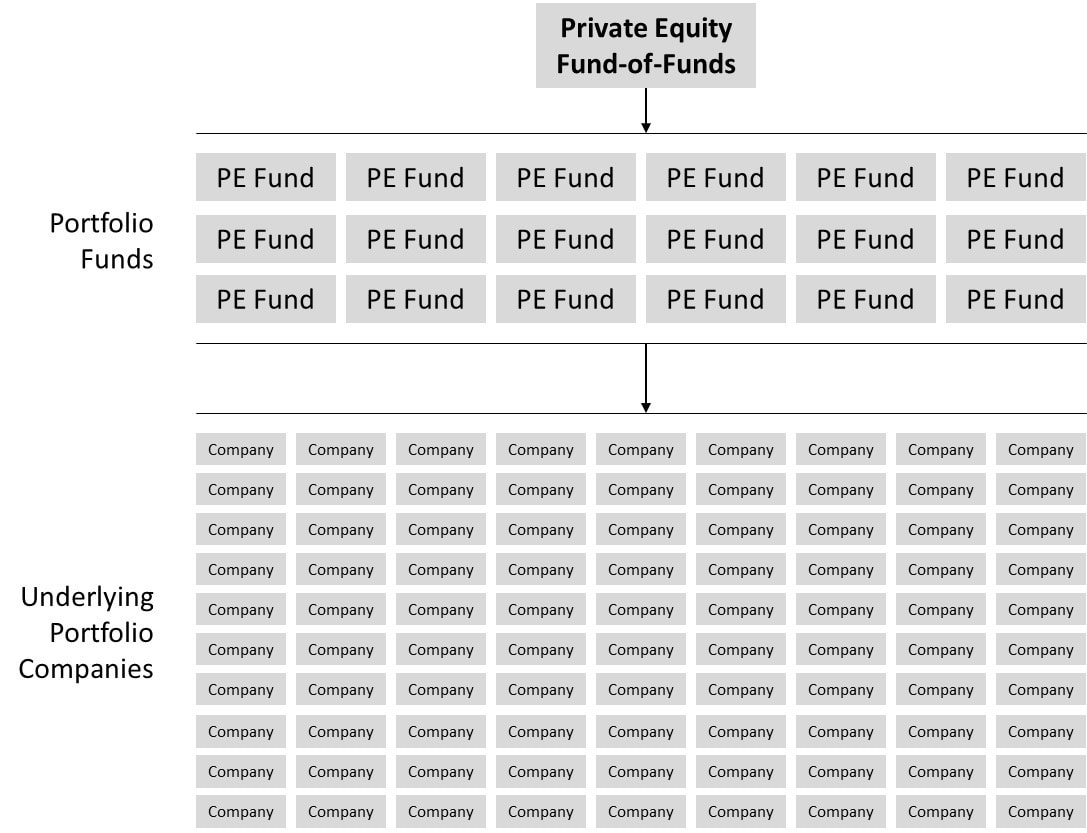

FOFs invest in a portfolio of private equity funds (known as “portfolio funds”), which in turn invest in privately-held companies (known as “underlying portfolio companies”). A FOF will invest in a portfolio of private equity funds and each portfolio fund will invest in a portfolio of private companies. As a result, an LP’s single investment in a FOF can provide the LP with exposure to many funds and potentially hundreds of underlying portfolio companies. The simplified diagram below illustrates this.

Private equity funds-of-funds (“FOFs”) are funds that invest in other private equity funds, which then invest directly into privately-held companies. By investing in a FOF, a limited partner (“LP”) obtains a diversified portfolio of private equity fund investments as well as a larger portfolio of indirect investments in underlying private companies. I have worked for two private equity fund-of-fund managers and understand well the pros and cons of these vehicles. This post provides an overview of FOFs.

Structure

FOFs invest in a portfolio of private equity funds (known as “portfolio funds”), which in turn invest in privately-held companies (known as “underlying portfolio companies”). A FOF will invest in a portfolio of private equity funds and each portfolio fund will invest in a portfolio of private companies. As a result, an LP’s single investment in a FOF can provide the LP with exposure to many funds and potentially hundreds of underlying portfolio companies. The simplified diagram below illustrates this.

Blind Pools and Target Lists. FOFs are usually “blind pools”, meaning that at the time the LP makes its commitment to the FOF, the identity of the funds in which the FOF will invest is not known. When an LP invests in a FOF the LP is relying on the expertise of the FOF manager to invest in high-quality, high-performing private equity funds. Some FOFs, such as those focusing on venture capital, may have a “target list” of fund managers that the FOF has identified as high-quality, high-performing managers, and that the FOF expects to invest in many of the funds of these managers. In some cases, if the FOF fails to invest in a minimum percentage of funds of the managers on the target list, the FOF manager will suffer a penalty, such as reduced carry. The idea of a target list is to give LPs comfort about the FOF’s ability to invest in funds where access may be limited – such as in top-performing venture capital funds.

Committed Capital Basis. Like the funds in which they invest, FOFs operate on a committed capital basis. For a detailed discussion of committed and called capital, see the post “LP Corner: On Committed Capital, Called Capital and Uncalled Capital.”

Legal Structure. Most US FOF vehicles are structured as Delaware limited partnerships, the same legal entity used by most private equity funds. For a detailed discussion of the limited partnership structure, see the post “LP Corner: US Private Equity Fund Structure – The Limited Partnership.”

Management Fees and Carry. FOFs generally usually charge a management fee ranging from 50 basis points (0.5%) per year to 100 basis points (1.0%) per year on committed capital (which fees usually ramp down over time). Most FOFs also charge carried interest (profit share, also known as carry) typically of about 5% (some charge more, or may have tiered carry). Many FOFs also have a preferred return hurdle. Because a FOF’s underlying portfolio funds also charge a management fee (usually around 2%) and carry (usually 20%), FOFs are often criticized for having a double layer of fees, or “fees on fees.” For a detailed discussion of fund management fees, see the post “LP Corner: Fund Terms – Management Fee” and for a detailed discussion of carry, see the post “LP Corner: Fund Terms – Carried Interest Overview.”

Investment Period. Many FOFs have an investment period of three to five years, meaning that the FOF will make its commitments to private equity funds over that period of time. However, there are many variations of this, with some FOFs having a one-year investment period.

Term and Extensions. The initial term of FOFs is generally 12 to 15 years, with several one-year extensions at the discretion of the general partner of the FOF (the “GP”). This is longer than the standard 10-year term with two one-year extensions of most private equity funds, and the longer term for FOFs reflects the fact that FOFs invest in funds over three to five years. So, if a FOF invests in a private equity fund in year 5, that portfolio fund will likely have a 10 year term plus two one-year extensions, which means that the FOF will be in existence for at least 17 years to match the term of the portfolio fund (unless it sells its interest in the portfolio fund in a secondary transaction). The ultimate life of a FOF can extend to 18-20 years because some of the underlying funds will continue to have a few remaining portfolio companies. For more information on private equity fund terms, please see my post “LP Corner: The Four Phases in the Life of a Private Equity Fund.” Note also that there are FOFs with an “evergreen” structure, meaning that the fund has an indefinite term and will continuously invest.

Strategy

Many large FOFs will have broad investment strategies, such as to invest in global buyout funds, growth funds, venture capital funds and private credit strategies. However, many FOFs have more specific strategies, such as focusing on a specific geography (Asia, Europe, the United States (or North America), South America, the Middle East, Africa, etc.), a specific strategy (venture capital, middle market buyouts, emerging managers, small funds, etc.), or a combination thereof. For example, there are many FOFs that focus on US venture capital strategies, and even FOFs that focus on sub-$100 million US venture capital funds.

While many FOF only invest in private equity funds, others will have the ability to invest in secondary fund opportunities and to co-invest alongside their portfolio funds in underlying portfolio companies. These additional strategies can increase returns and also help to mitigate the impact of the J-Curve. For a detailed discussion of the J-Curve, see the post “LP Corner: The J-Curve.”

Reasons to Invest in a FOF

There are many reasons to consider investing in a FOF:

- Potential for attractive risk-adjusted return. FOF managers are experts in investing in private equity funds. This, combined with the diversification benefits (discussed below) that a FOF provides, can lead to attractive risk-adjusted returns. There is research that supports this, for example Harris et al., “Financial Intermediation in Private Equity: How Well Do Funds of Funds Perform?” by Robert S. Harris, Tim Jenkinson, Steven N. Kaplan and Ruediger Stucke, NBER May 2017. Here’s a link to the paper: https://www.nber.org/papers/w23428.pdf

- Diversification benefits. A FOF provides diversification across private equity funds and underlying portfolio companies. This diversification can reduce risk while also optimizing potential return. In addition, diversification also provides protection against downside risk. A research article that explains this well is “The Risk Profiles in Private Equity” by Tom Weidig and Pierre-Yves Mathonet published in 2004. While a little dated, I think the general principles are still valid. Here’s a link to the paper: https://ssrn.com/abstract=495482

- Expert Investors. FOF managers will have expert investment teams that have significant experience in identifying and investing in top-performing private equity funds. Also, most established FOF managers have extensive databases of information on their portfolio funds as well as target funds. This data can be extremely useful in evaluating funds. Many smaller LPs will not have this type of focused expertise.

- Access to a Specific Strategy or Geography. As discussed above, many FOF are specialist funds, focusing on a particular strategy such as venture capital or lower middle market buyouts, or on a specific geography, such as Asia or Latin America. The expertise of the FOF manager in these strategies or geographies is difficult to replicate by most LPs without the help of an external advisor. In my view, FOFs for venture capital strategies are particularly interesting, as the FOF manager will have developed relationships with leading venture capital firms whose funds are heavily sought after and the firms are able to limit access to the fund to certain LPs.

- Administrative Efficiency. Managing capital calls and distributions can be an administrative burden to an LP, especially for a smaller LP or one that is new to private equity investing. Because the FOF handles all of the capital calls and distributions from its portfolio funds, the LP only has to manage the capital calls and distributions from the FOF. Also, some private equity funds (primarily venture capital funds) will distribute stock of their portfolio companies to LPs after the company has gone public. Managing these stock distributions (also known as “in-kind” or “in-specie” distributions), can be an administrative burden for some LPs, particularly smaller LPs. Many FOFs offer a cash-in-cash-out strategies, which means the LP does not have to manage in-kind distributions.

- Single Investment Provides Access to Many Funds. Many top private equity funds have a minimum LP investment of $5 million, or more. To build a diversified portfolio of private equity funds, an investor would need to be able to commit a significant amount of capital. However, by investing in a FOF, a single investment will provide the investor with a diversified portfolio of private equity funds for a fraction of the cost of investing in the funds directly.

- Good Entry Point to Private Equity. FOFs are a good way for an LP new to private equity to start their investment program and to learn the mechanics of private equity. FOFs will have annual investor meetings, where they often invite their portfolio fund managers to speak, and these investor meetings are a great way for a new LP to meet fund managers as well as other LPs. As an LP becomes more experienced as an investor in private equity, it can move to investing directly into funds. After another period of time, the LP can begin to invest in co-investments and in direct investments.

Issues to Consider

The following are some issues relating to investing in FOFs:

- Fees on fees. As discussed above, most FOFs charge a management fee and carry. However, because the FOF management fee includes the costs of administering all of the underlying portfolio investments, the fees paid to a FOF can be lower than building an internal private equity investment staff.

- Potentially Lower Returns. Because of the built-in diversification that a FOF offers, it follows that the return profile for a fund-of-fund will be different than investing directly into a private equity fund. While a FOF provides more protection against downside returns, the cost of this protection is that the FOF may also provide lower returns than an investment directly into a private equity fund.

- Portfolio Fund Relationships with FOF Manager. The FOF manager has direct relationship with its portfolio fund managers, because it is the FOF manager that is sourcing and evaluating the managers and managing the FOF’s investments in the portfolio funds. As a result, the relationship an LP in the FOF has with the underlying fund managers will be more indirect. Having said that, many FOF managers understand that a FOF may be a stepping stone for an LP new to the private equity industry, and so the FOF manager may accommodate the LP and make introductions to the portfolio fund managers.

- Longer terms. As discussed above, the terms for FOFs are generally longer than the term of an individual private equity fund. Having said that, if an LP were to invest directly in private equity funds directly over a period of years, that LP would face the same issue of fund terms.

- Deeper, Longer J-Curve. A FOF, particularly one focused on investing in early-stage venture capital funds, may experience a deeper and longer J-Curve. For more information on the J-Curve, please see my post “LP Corner: The J-Curve.”

- Less Visibility on Underlying Portfolio Companies. Because FOFs invest in a portfolio of funds, the information provided to the LPs on the underlying portfolio funds may be more “high level” and not provide much information on the underlying portfolio companies. LPs investing directly in funds may obtain more detailed information on the fund’s portfolio companies.

- Illiquid Investment. An investment in a FOF is illiquid - meaning that there is no readily available public market where the LP can sell its interest in the FOF. There is however a broad "secondary market" for the private sale of private equity fund interests, including FOF interests. This secondary market is less efficient than a public market would be. In addition, the secondary market for FOF interests generally offers less liquidity than for private equity fund interests, because there are less buyers for these types of interests. This means that an LP looking to sell its FOF interest on the secondary market may have to sell its interest at a larger discount to Net Asset Value (the carrying value of the LP's interest in the FOF) than if there were a more robust market for FOF secondaries.

When Investing in FOFs Makes Sense

Investing in FOFs makes sense in the following situations:

- New to Private Equity. FOFs are a good way for investors new to private equity to obtain exposure to the asset class. For new investors, an investment in a FOF may be complemented by an investment in a secondary fund, as a secondary fund can help to shorten the J-Curve.

- Smaller Programs. If an investor does not have sufficient capital to invest directly in a portfolio of funds, an investment in a FOF may be a good way to obtain access to the private equity asset class.

- Complement to Existing Program. A FOF can be a complement to an existing program, for example, to provide access to venture capital that may not otherwise exist in the program.

- Specific Mandates. A FOF is also a good way to “fill-in” an existing program. For example, if a private equity program has made investments in US private equity funds, but has no foreign exposure, investing in a non-US FOF might be a good way to access these geographies and strategies.

- Access to Venture Capital. As an example of a specific mandate, a FOF can be a good way to access venture capital, where access to the best-performing funds can be extremely limited. Investing in a FOF can be a way to obtain access to these top-performing venture capital funds.

© 2019 Allen J. Latta. All rights reserved.