Have you heard the term “ROFR” (pronounced “Roafer”)? This term is well known by professional investors.

ROFR means Right of First Refusal. We will do a deep dive on ROFRs in this post.

ROFR means Right of First Refusal. We will do a deep dive on ROFRs in this post.

ROFRs apply when an existing investor in a company wants to sell some or all of its shares in the company. If this investor receives an offer from a potential buyer for its stock, the ROFR prevents this investor (known as a “selling stockholder”) from just going ahead and selling its stock to the potential buyer. The ROFR requires the selling stockholder to offer to sell its shares to the company and/or the other stockholders at the same price and other terms proposed by the potential buyer. If the company and/or the other stockholders buy all of the stock being sold by the selling stockholder, then the potential buyer loses out. If, however, the company and/or the other stockholders don’t buy all of the stock being sold by the selling stockholder, then the selling stockholder can go ahead and sell to the potential buyer.

ROFRs are very common in venture capital financings. Venture capital investors want ROFRs so that if an existing investor wants to sell some or all of its stock, the other investors can buy this stock.

Mechanics

The way a ROFR works is that if an investor (the “selling stockholder”) receives an offer from a potential buyer (called a “third party”) to purchase some or all of its shares, then that selling stockholder must notify the company and the other investors about the offer, including the number of shares the investor wants to sell (called the “offered shares”), the price and all other terms of the offer. The company then has a period of time, usually 15 days, to decide how many of the offered shares the company wants to buy, which can be all, some or none.

Company Buys All Offered Shares. If the company decides to buy all of the offered shares, then that’s what happens and the ROFR process ends. The selling stockholder sells all of the offered shares to the company for on the same terms that were offered by the potential buyer. The potential buyer loses out.

Company Buys Some or None of the Offered Shares. If the company decides to buy some, but not all, of the offered shares, or decides to buy none of the offered shares (which is common), then the company notifies the selling stockholder and the other investors of the number of shares the company is buying. The other investors then have the right to purchase the remaining shares on the same terms offered by the potential buyer. When the company notifies the other investors of the total number of offered shares available to purchase, the company includes in the notice the number of offered shares each stockholder can buy, which is based on the “pro rata” or proportionate ownership of the investors that are covered by the ROFR.

The stockholders then have a short period of time after receiving the notice from the company, usually 10 days, to decide they will buy the shares offered to it. Typically, they have to buy all shares offered to them, or none; they can’t buy some of the shares offered to them. If one or more stockholders don’t buy their allotment of offered shares, then the company will send another notice to the stockholders who indicated that they will buy their allotment, and these stockholders can then pick up the slack.

After going through this process, the company and the stockholders have to indicated that they will buy all of the offered shares. If the company and the stockholders don’t indicate that they will buy all of the offered shares, then they lose the right to buy any of the offered shares and the selling stockholder will then sell the offered shares to the potential buyer.

Notes

Example

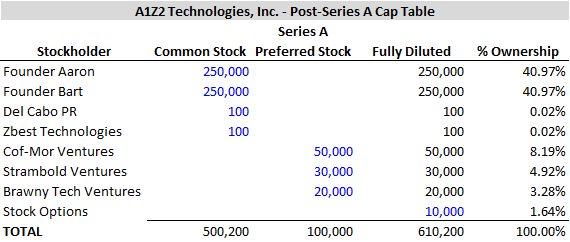

A1Z2 Technologies, Inc., an early-stage enterprise software company, has 2 founders who each own 250,000 shares of common stock. The company also issued 100 shares of common stock to two vendors who took stock in exchange for services. The company then held a Series A Convertible Preferred Stock financing and raised $1 million from three venture capital firms. In this Series A financing, the company issued 100,000 shares of Series A preferred stock to three investors at $10.00 per share. The company also has a stock option pool of 50,000 shares, of which 10,000 have been granted. Here’s the post-Series A cap table:

ROFRs are very common in venture capital financings. Venture capital investors want ROFRs so that if an existing investor wants to sell some or all of its stock, the other investors can buy this stock.

Mechanics

The way a ROFR works is that if an investor (the “selling stockholder”) receives an offer from a potential buyer (called a “third party”) to purchase some or all of its shares, then that selling stockholder must notify the company and the other investors about the offer, including the number of shares the investor wants to sell (called the “offered shares”), the price and all other terms of the offer. The company then has a period of time, usually 15 days, to decide how many of the offered shares the company wants to buy, which can be all, some or none.

Company Buys All Offered Shares. If the company decides to buy all of the offered shares, then that’s what happens and the ROFR process ends. The selling stockholder sells all of the offered shares to the company for on the same terms that were offered by the potential buyer. The potential buyer loses out.

Company Buys Some or None of the Offered Shares. If the company decides to buy some, but not all, of the offered shares, or decides to buy none of the offered shares (which is common), then the company notifies the selling stockholder and the other investors of the number of shares the company is buying. The other investors then have the right to purchase the remaining shares on the same terms offered by the potential buyer. When the company notifies the other investors of the total number of offered shares available to purchase, the company includes in the notice the number of offered shares each stockholder can buy, which is based on the “pro rata” or proportionate ownership of the investors that are covered by the ROFR.

The stockholders then have a short period of time after receiving the notice from the company, usually 10 days, to decide they will buy the shares offered to it. Typically, they have to buy all shares offered to them, or none; they can’t buy some of the shares offered to them. If one or more stockholders don’t buy their allotment of offered shares, then the company will send another notice to the stockholders who indicated that they will buy their allotment, and these stockholders can then pick up the slack.

After going through this process, the company and the stockholders have to indicated that they will buy all of the offered shares. If the company and the stockholders don’t indicate that they will buy all of the offered shares, then they lose the right to buy any of the offered shares and the selling stockholder will then sell the offered shares to the potential buyer.

Notes

- Limited to Major Investors. ROFRs are usually limited to major investors. The reason for this is that if the company has a lot of stockholders, going through the ROFR process is very complex and burdensome.

- Stock Options Excluded. ROFRs don’t cover stock options or warrants. Only major investors who own lots of common or preferred stock have the ROFR.

- Excluded Transfers. ROFRs are designed to cover all transfers of stock, but there are a few exemptions. Venture capital funds sometimes need to transfer the stock to an affiliate (such as a different fund managed by the venture capital firm), and so these types of transfers are often allowed.

- Non-Cash Consideration. Sometimes a prospective buyer will offer a selling stockholder something other than cash for the offered shares. Sometimes this can be shares of stock of another company, services or some type of property. In this case, the company’s board of directors determines the fair market value of this non-cash consideration, and the company and stockholders can pay cash based on this fair market value.

- Variations. There are many variations to ROFRs. One company-favorable variation is where the ROFR is an exclusive right of the company and not the other stockholders. The company can exercise its right, can waive it, or can assign (transfer) it to one or more stockholders. But similar to above, if the right isn't exercised within a certain period of time, then the right terminates and the transaction can occur. This variation makes it easier for the company to approve secondary sales by existing stockholders if it wants to do this for an existing officer or employee. This variation also give the company more control over its capitalization table. If there's a stockholder that's been really helpful to the company, the company can assign its ROFR to this stockholder to reward this stockholder.

- Documents. The ROFR can be its own separate agreement, or the ROFR can be contained in a stockholder agreement or investor agreement.

- Co-Sale Rights. It is common for ROFRs to be paired with co-sale rights, which apply if a ROFR is not exercised, and enable other stockholders to participate in the sale. We sill discuss co-sale rights in a future post.

Example

A1Z2 Technologies, Inc., an early-stage enterprise software company, has 2 founders who each own 250,000 shares of common stock. The company also issued 100 shares of common stock to two vendors who took stock in exchange for services. The company then held a Series A Convertible Preferred Stock financing and raised $1 million from three venture capital firms. In this Series A financing, the company issued 100,000 shares of Series A preferred stock to three investors at $10.00 per share. The company also has a stock option pool of 50,000 shares, of which 10,000 have been granted. Here’s the post-Series A cap table:

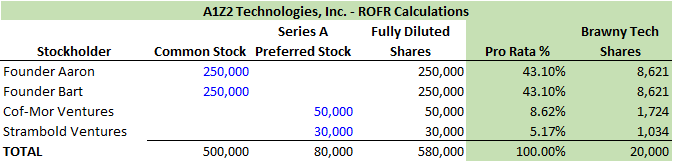

As part of the Series A financing, the investors obtained a ROFR that covered all investors owning 20,000 shares or more (“major stockholders”). This means the founders and the venture capital investors are covered by the ROFR. The two vendors (with 100 shares each) and the stock options are excluded from the ROFR. The ROFR provides that the company and the other stockholders have the right to purchase any offered shares at the price and on the other terms of any offer.

A year later, Brawny Tech Ventures receives an offer from Really Smart Ventures to buy all of Brawny Tech’s 20,000 Series A shares for $50.00 each in cash. This offer is five times what Brawny Tech paid and would be a great return for Brawny Tech. Brawny Tech sends a notice to the company about the offer. The company decides not to buy any of the offered shares. Because of this, the major stockholders have the right to buy all of Brawny Tech’s 20,000 on a pro rata (proportionate basis). The table below shows the pro rata amounts and the number of Brawny Tech shares each major investor can purchase:

Each investor buys their pro rata portion of Brawny Tech’s shares at the $50.00 cash price. Because the ROFR has been exercised in full, Really Smart Ventures loses out.

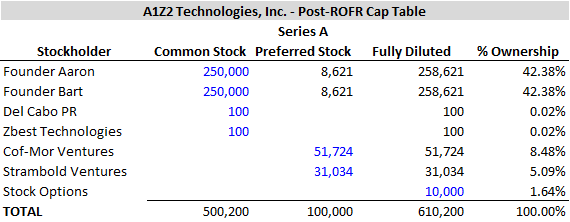

Here’s the cap table after the ROFR:

Here’s the cap table after the ROFR:

Let’s check this. First, the number of shares of common stock outstanding before and after the ROFR remain the same. This is correct. Only shares of Series A Preferred Stock were sold. Second, the number of Preferred Stock outstanding before and after the ROFR remain the same. What has changed is the number of Series A shares each investor owns. The founders each purchased 8,621 shares of Series A stock from Brawny Tech Ventures, and Cof-Mor Ventures and Strambold Ventures purchased 1,724 and 1,034 shares of Series A stock from Brawny Tech Ventures. Finally, the number of fully diluted shares (610,200) didn’t change. This is correct. All that happened was that Brawny Tech sold its shares to existing stockholders and not the company. If the company had purchased shares, the shares the company purchased would be retired and this would reduce the number of shares outstanding.

I hope post has helped your understanding of ROFRs. If so, give it a Like!

© Allen J. Latta. All rights reserved.